Common Ground Health CO-OP has Exceeded Enrollment Targets, but Finished Last Year $36 Million in the Hole

August 6, 2015

[Milwaukee, Wisc…] A Wisconsin non-profit health insurer set up by the Affordable Care Act (ACA) that received $108 million in loans from the federal government finished 2014 with a $36.5 million deficit, according to a report from the Inspector General’s office of the Department of Health and Human Services (HHS).The large net operating loss for Common Ground Health Care Cooperative came despite their ability to exceed enrollment projections by almost three-fold.

Deep in the morass of Obamacare is a state-based health care market program called Consumer Operated and Oriented Plans (CO-OP). The CO-OP program is intended to provide a low cost, nonprofit health care alternative to commercial insurance plans in each state that they operate in.

A CO-OP health care agency must be a consumer group, community organization, medical provider organization, union or a business coalition. For-profit businesses are blocked from participating because of the program’s mission to direct all revenue generated back to setting lower premiums or improving quality of care.

Originally, the ACA allocated $6 billion for start-up and solvency loans for the CO-OP program with the hope of establishing one in each state. However, only 23 CO-OPs were started, and four of those are set up to serve two states.

The total amount of funds that made it out to the CO-OPs was slashed to $2.4 billion because of some early warning signs and bad results in the first few years.

The HHS Inspector General’s office first raised concerns about CO-OPs in 2013, citing little private money support and that many CO-OPs were burning through their start-up loans.

In February 2014, the House Committee Oversight Committee expressed plenty of reservations about the program, whose report’s findings are worth quoting:

“The Committee’s examination of ObamaCare’s Consumer Operated and Oriented Plan (CO-OP) program reveals that the program has jeopardized up to $2 billion in federal taxpayer money. The ongoing oversight has uncovered numerous examples in which companies selected to receive CO-OP loans are plagued with legal and financial issues. The Committee’s oversight has also shown that the companies receiving CO-OP loans oftentimes have strong political ties to the Obama Administration. The Committee’s findings to date raise troubling questions, not only about the administration of the CO-OP loan program, but also about the effectiveness of ObamaCare implementation in general. By the Administration’s own projections, taxpayers should expect to lose over 40 percent of the amount of loans paid out through the CO-OP program.”

Then came the failures.

An attempt to start a CO-OP in Vermont was shut down by state regulators in 2013 because of its inability to show how it would stay solvent.

The Iowa/Nebraska joint CO-OP, CoOportunity Health, is perhaps the worst failure so far. After receiving $145 million in start-up loans and greatly exceeding enrollment targets, CoOportunity Health found itself with total losses $168 million by January 2015. A few weeks later, the CO-OP was liquidated and 120,000 enrollees were forced to find coverage elsewhere.

Now, CoOportunity Health may not come up with the cash to pay the federal government back.

Just recently, the Louisiana state insurance office announced that its CO-OP program would be shutting its doors at the end of the year. The Louisiana CO-OP installment had failed to meet enrollment targets for the end of 2014 and had burned through most of its $66 million federal loan before officials decided that it did not have the ability to stay solvent. In fact, an insurance rating agency had reported an indebtedness of 198 percent through the third quarter of 2014 for the program.

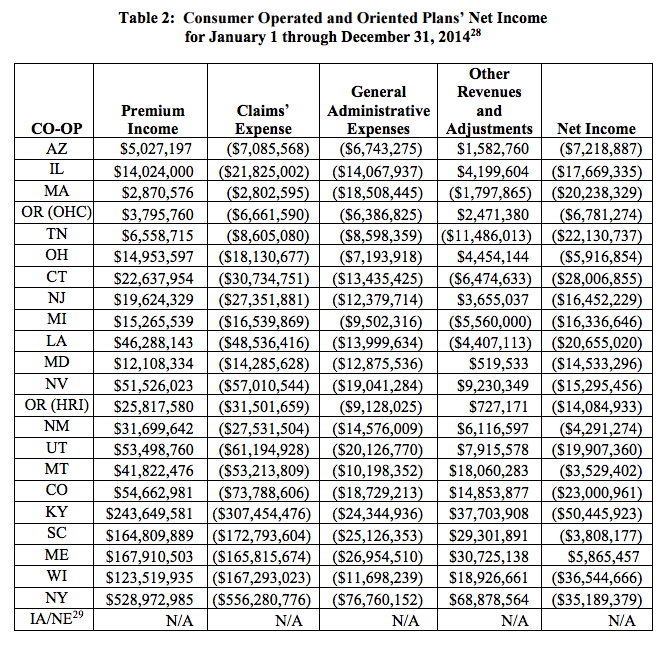

Many other CO-OPs look to be in danger of going belly up. An analysis by the National Association of Insurance Commissioners warns of financial trouble and pegs combined 2014 net losses for the remaining CO-OPs at $389 million.

Another study by the HHS Inspector General shows that over half of the 23 CO-OPs have failed to meet their enrollment targets by the end of 2014 and all but one (Maine) finished last year deep in the red.

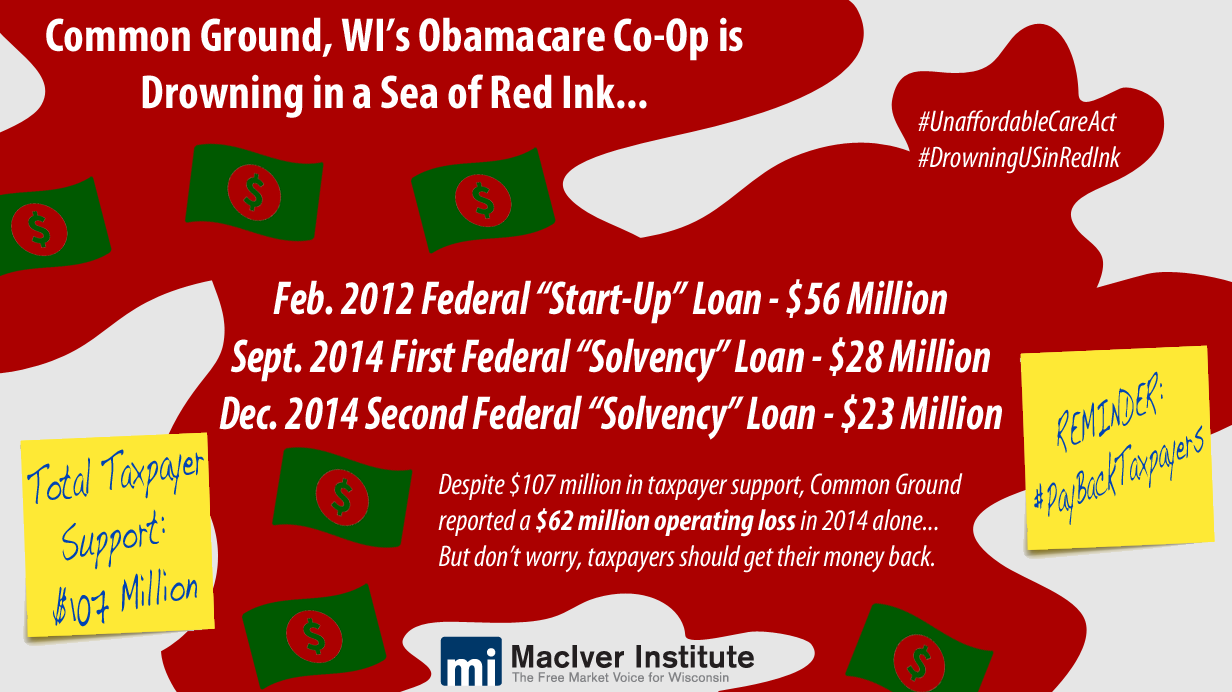

Wisconsin’s CO-OP program, Common Ground, was awarded $56.6 million in federal start-up loans in 2012 and 2013 and then received $51 million in additional solvency loans in 2014. Common Ground did greatly exceed enrollment targets by the end of 2014, enrolling 26,000 when they only expected 10,000.

However, despite the overwhelming success Common Ground has experienced in enrolling people, the agency is drowning in red ink. Net income losses of $36.5 million for Common Ground in 2014 was $35 million more than was expected.

In addition, according to the Galen Institute, Common Ground actually faced a $62 million operating loss in 2014 when Risk Corridor Receivables were not counted. The Risk Corridor was created by the ACA to take money from profitable insurance companies and give it to unprofitable ones.

However, a Standard and Poor’s report claimed there would not be enough money to cover the deficits from groups like Common Ground.

“We estimate that the ACA risk corridor will not receive adequate monies from insurers with profitable exchange business to pay insurers that have unprofitable exchange business,” the report read.

Common Ground’s net income loss was second highest among the 23 CO-OPs, with the Kentucky Health Cooperative finishing last $50.5 million in the hole.

The Inspector General’s office sums up why so many CO-OPs are experiencing such great shortfalls.

“Claims’ expense exceeding premium income can be attributed to higher than estimated enrollment of members with more expensive health conditions, enrolling fewer-than expected young and healthy members, or inaccurate pricing of health insurance premiums.”

Common Ground also went through a leadership overhaul in the middle of its first full year of operation. According to the new CEO Cathy Mahaffey, something had not gone right in the claims division.

“We had some bumps with our claims administrator,” Mahaffey said. “We had delays in claims processing. They have been cleared out only recently.”

Common Ground also introduced a new eight-member board at the start of 2015.

According to the Inspector General’s report, Common Ground has set a slightly positive net income target for the end of 2015 and $3.35 million worth of positive income in 2016. Meeting its 2015 goals would require a $37 million swing for the agency.

As several CO-OPs slip into financial turmoil around the nation, taxpayers should be aware of how their money is being wasted.